Abstract: China's IC industry has been flourishing in recent years, huge market demand together with government investments are the major driving forces for this development. The status and development momentum of the Chinese IC industry also attracted wide interest and attention of international counterparts. A group of domestic IC experts are invited by the JoMM to write a series of articles about China's IC industry, including the history, current status, development, and related government policies. Information in these articles is all from public data from recent years. The purpose of these articles is to enhance mutual understanding between the Chinese domestic IC industry and international IC ecosystem.

Keywords: IC industry; Integrated Circuit Design Market

1. China's Integrated Circuit Industry Continues to Develop Fast

With the rapid development of the global electronic information industry, the global integrated circuit design industry has been showing a trend of continuous growth. Although China's integrated circuit design industry started late, with the stable development of the national economy and the introduction of a series of favorable policies, coupled with huge market demand, it has become the main driving force for the growth of the global integrated circuit design industry market.

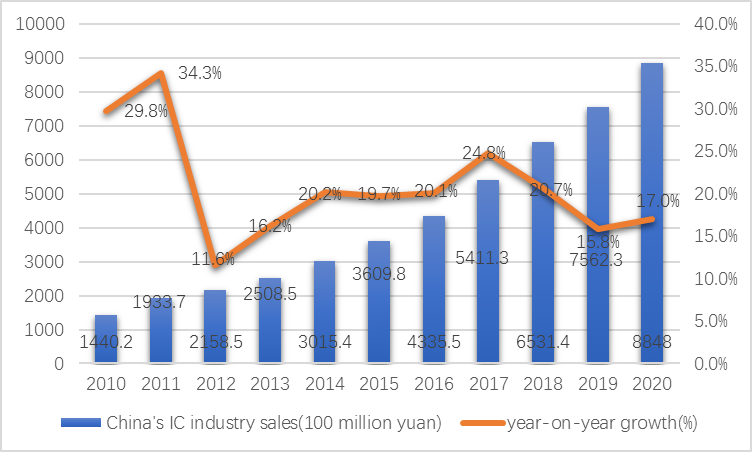

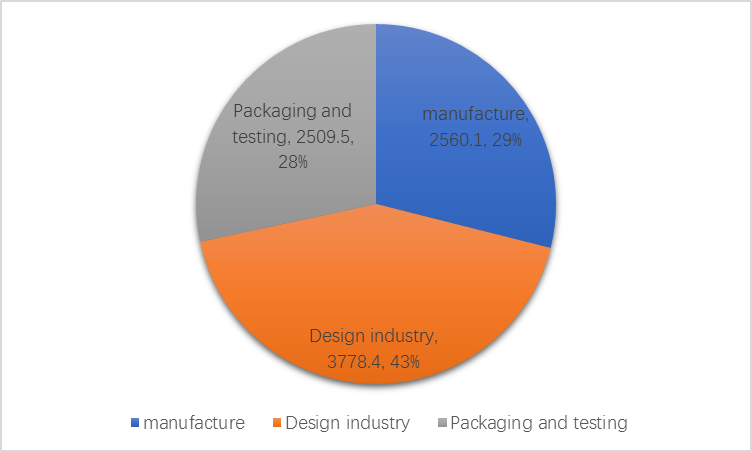

According to the statistics from the China Semiconductor Industry Association, the overall sales of China's integrated circuit industry from 2010 to 2019 showed an overall growth trend, from 144.015 billion yuan in 2010 to 756.23 billion yuan in 2019, which was mainly driven by the downstream market demand of Internet of Things, smart cars, new energy vehicles, smart terminal manufacturing and new generation mobile communication. In 2020, China's integrated circuit industry sales continued to maintain double-digit growth, with annual sales reaching 884.8 billion yuan, 17% increase from 2019. Among them, the sales of the design industry reached 377.84 billion yuan, an increase of 23.3% year-on-year. It is still the fastest growing industry in the "three industries" of design, manufacturing and packaging and testing, accounting for 42.7% of the overall industry; sales of manufacturing were 256.01 billion yuan, an increase of 19.1%year-on-year, accounting for 28.9%; Sales volume of packaging and testing industry was 250.95 billion yuan, an increase of 6.8%year-on-year, accounting for 28.4%.

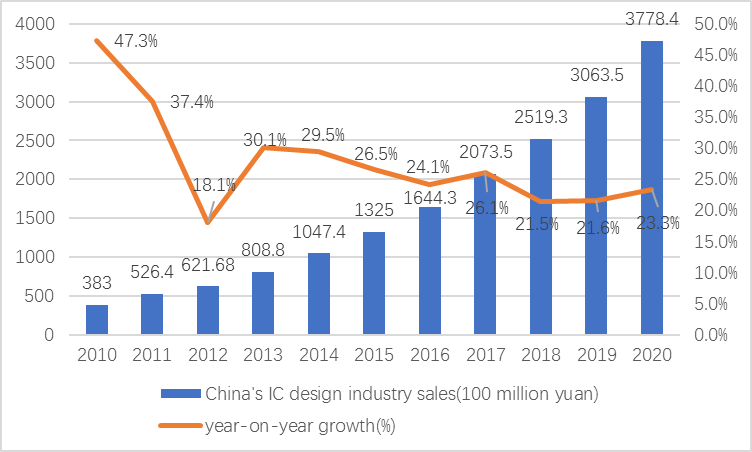

Figure 1.

2010-2020 China's IC market sales trend. Figure 2.

2020 China's integrated circuit industry segments sales distribution. In addition, according to the statistics of the National Bureau of Statistics, our country’s integrated circuit production will increase year by year from 2010 to 2020, from 65.25 billion in 2010 to 100 billion in 2014 for the first time to 200 billion for the first time in 2019. In 2020, China's IC output reached 261.26 billion pieces, a year-on-year increase of 29.5%, and the output hit a new high.

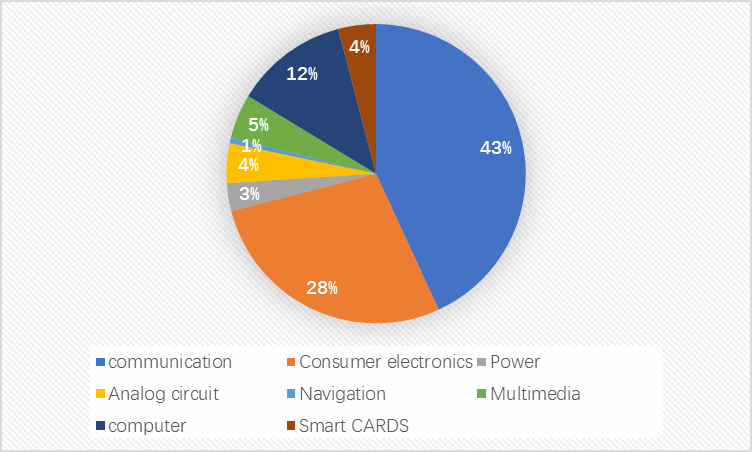

In terms of product applications, in 2020 the largest product application field in China's integrated circuit design industry is the communication field, the total sales in the communication field is 164.71 billion yuan, accounting for 43%; Followed by the field of consumer electronics, with the sales of 106.39 billion yuan, accounting for 28%; the sales of computer is 46.73 billion yuan, accounting for 12%, ranking third.

Figure 3.

2020 China's IC design industry product distribution by applications (%). 2. The Scale of China's Integrated Circuit Design Market Continues to Expand

In recent years, driven by national policy support and market application, China's IC industry has maintained rapid growth and continued to maintain the global leading momentum in growth rate. Driven by this, in the development of the domestic IC industry, the IC design industry has always been the most dynamic field in the domestic IC industry, with the fastest growth. According to the statistics of China Semiconductor Industry Association, the sales revenue of integrated circuit design industry increased from 38.30 billion yuan in 2010 to 306.35 billion yuan in 2019, the market scale continued to expand, and the overall growth rate was considerable. Except for 2012, the annual growth rate of the industry market exceeded 20%. By the end of 2020, the market size of China's IC design industry has reached 377.84 billion yuan, a year-on-year increase of 23.3%.

Figure 4.

2010-2020 China's IC design market sales trend. With the issuance of ‘The Outline of National Integrated Circuit Industry Development Promotion’ and a series of other encouraging policies, the integrated circuit design industry has become the most competitive field in China's integrated circuit industry. Since 2015, local governments have adopted various preferential measures to attract domestic mature design companies to open branches in different places. According to the statistics of the Integrated circuit Design Branch of China Semiconductor Industry Association, there were 2218 domestic chip design companies in 2020, 438 more than the 1780 in 2019, and the number increased by 24.6%. In addition to the gathering places of traditional design enterprises such as Beijing, Shanghai and Shenzhen, there are more than 100 design companies in Wuxi, Hangzhou, Xi 'an, Chengdu, Nanjing, Wuhan, Suzhou, Hefei and Xiamen.

China's IC design industry has not only improved the number of enterprises, but also made remarkable achievements in the quality of development. For example, the rapid rise of design companies focusing on emerging markets means that Chinese mainland IC design companies have gradually approached the world leading level.

3. The Competitive Landscape of China's IC Design Market

According to the top ten domestic IC design companies published by China Semiconductor Association in 2019, the rankings are Huawei HiSilicon, Howe Group, IPCore Microelectronics, Huada Semiconductor, UNIS Spreadtrum, Huada Semiconductor, Goodix, Galaxycore, Hangzhou Silan, Beijing Zhaoyi. In 2020, China's top ten IC design companies have not announced their names. However, its distribution area was announced, and its distribution was 3 in Pearl River Delta region, 6 in Yangtze River Delta and 1 in Beijing-Tianjin-Bohai Rim Sea region.

Table 1.

2019 China's IC design industry's top 10 companys. | Ranking | Company Name |

| 1 | HiSilicon |

| 2 | Howe Group |

| 3 | IPCore Microelectronics |

| 4 | Huada Semiconductor |

| 5 | UNIS Spreadtrum |

| 6 | Huada Semiconductor |

| 7 | Goodix |

| 8 | Galaxycore |

| 9 | Hangzhou Silan |

| 10 | Beijing Zhaoyi |

The overall growth rate of the top ten design enterprises is 20%, which is 3.8 percentage points lower than the average growth rate of the whole industry. The threshold for entering the top ten integrated circuit design enterprises has increased from 4.8 billion in 2019 to 4.85 billion in 2020; In 2020, the sales of the top ten design enterprises totaled 186.89 billion yuan, accounting for 48.9% of the industry scale, which was 1.2 percentage points lower than the 50.1% in 2019, but compared with 40.21% still has a significant expansion.

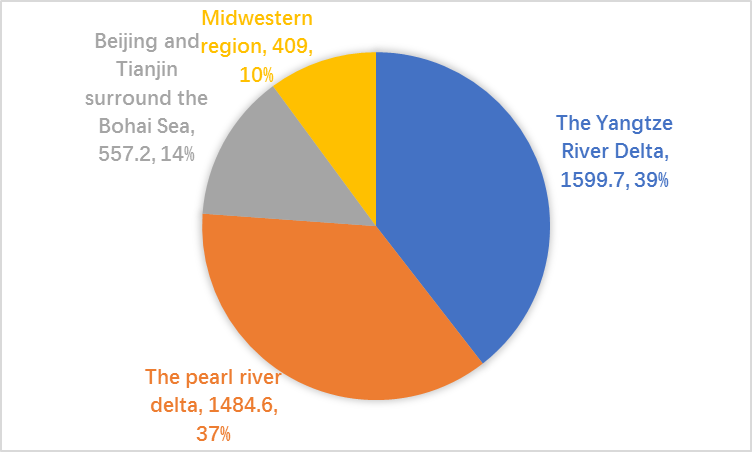

From the perspective of regional development of IC design industry, according to the data released by IC Design Branch of China Semiconductor Industry Association, in 2020, the sales volume of IC design industry in Yangtze River Delta region was 159.97 billion yuan, up 46.3% year-on-year, accounting for 39% of the whole country, and that in Pearl River Delta region was 148.46 billion yuan, up 17.7% year-on-year, accounting for 37% of the whole country. Sales of integrated circuit design industry in Beijing-Tianjin-Bohai Rim region reached 55.72 billion yuan, down 11.1% year-on-year, accounting for 14% of the whole country, while sales of integrated circuit design industry in central and western regions reached 40.9 billion yuan, up 41.7% year-on-year, accounting for 10% of the whole country.

Figure 5.

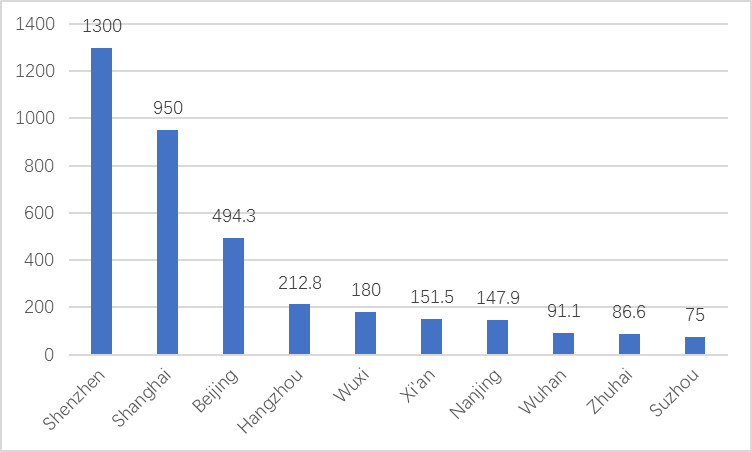

2020 China's IC design industry sales by region (100 million yuan, %). According to the data published by IC Design Branch of China Semiconductor Industry Association, the top ten cities in terms of IC design sales in 2020 are Shenzhen, Shanghai, Beijing, Hangzhou, Wuxi, Xi 'an, Nanjing, Wuhan, Zhuhai and Suzhou, among which the IC design sales in Shenzhen is 130 billion yuan. The sales volume of integrated circuits in Shanghai is 95 billion yuan, and the sales volume of integrated circuit design industry in Beijing is 49.43 billion yuan. Shenzhen, Shanghai and Beijing continue to hold the top three positions.

Figure 6.

2020 China's IC design industry sales by city (100 million yuan). 4. International Competitiveness of China's IC Design Industry

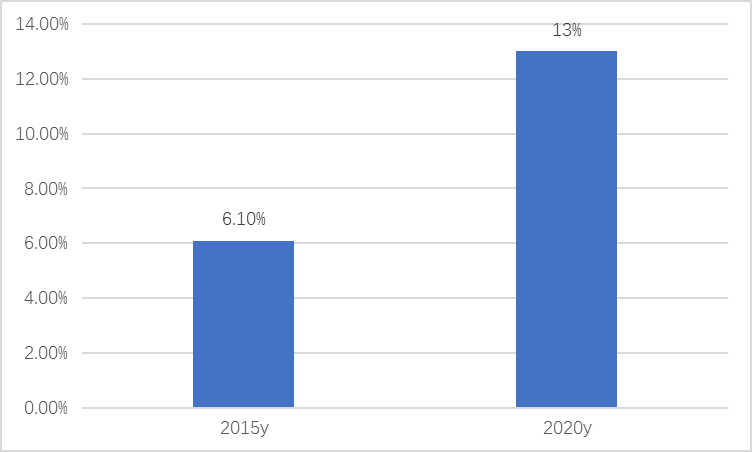

From the perspective of global regions, China's IC design industry is playing an increasingly important role in the world. In 2020, the sales share of China's IC design industry in the world will increase to about 13%, while in 2015 it will only be 6.1%.

Figure 7.

2015 vs. 2020 domestic integrated circuit design market sales accounted for the proportion of the global situation (%). In terms of global IC design enterprise competition, according to Trend Force statistics, Qualcomm's revenue in Q3 quarter of 2020 reached 4.967 billion US dollars, an increase of 37.6% year-on-year; Broadcom ranked second, with revenue of 4.626 billion US dollars, NVIDIA, MediaTek and AMD ranked third, fourth, and fifth respectively, Huawei unfortunately dropped fell out of the top ten.

5. Development Prospect and Trend of China’s Integrated Circuit Design Industry

In 2020, Covid-19 epidemic and other unfavorable factors appeared, which had a significant negative impact on the global economy, but the integrated circuit industry showed strong resilience. As one of the most dynamic regions in the development of the global integrated circuit industry, China has achieved good results, especially in the field of integrated circuit design:

Great progress has been made in the field of high-end chips. Although there are still some gaps between the domestic general-purpose CPU and the world's most advanced level, it has gone from "basically unusable" 10 years ago to "completely usable" today. The application of domestic CPUs began to shift from the dedicated field to the open market field, which is an important step with milestone significance. Domestic embedded CPUs has achieved the competition with foreign products on the same stage, from the previous dedicated-oriented to current general-purpose, with an annual sales reaching hundreds of millions. Domestic semiconductor memory has achieved zero breakthrough, 3D flash memory and DRAM have entered mass production, and the technology is close to the international advanced level. Domestic FPGA chips have fully entered the communications and complete machine markets, playing a decisive supporting role at critical moments. In the field of domestic EDA tools, a series of important single-point tools have been formed in the digital circuit flow after the simulation full-process design tools entered the market to compete. After several years of efforts, I believe that our country can also have its own digital circuit full-process tools.

The level of research and development continues to improve. During the "13th Five-Year Plan" period, the R&D level of China's chip design industry has been continuously improved. While the industry continues to make progress, the improvement of chip design technology is also remarkable. Previously, papers from China were rarely seen in ISSCC, an Olympic international academic conference in the field of chips, but there were positive changes during the 13th Five-Year Plan period. According to the latest news, at the ISSCC conference to be held next year, the number of employment papers in Chinese mainland surpassed that in Japan and Taiwan Province, China, reaching 21, an increase of 40% over 2020. Compared with the United States, which ranks first in the world, there is a big gap in the total number of papers, the proportion of industrial contributions and the actual employment ratio, but it has made great progress compared with the past. From 2016 onwards, the number of papers collected by Chinese mainland in the forum increased by 114% annually, the number of first authors increased by 78% annually, the number of technical fields covered increased from 5 to 10, and the number of invited technical judges also increased from 4 to 10. It fully demonstrates the remarkable achievements in the research work in the field of chip design in China.

Despite a series of achievements, there are still many problems to in our country’s IC design industry that need to be improved:

There is still a big gap between the development and demand of China's chip design industry. Despite rapid progress, "strong demand and insufficient supply" will still be a long-term challenge for China's integrated circuits. The foundation of long-term sustainable development of the industry is still weak. The achievements of the design industry in 2020 are related to the special environment such as COVID-19 epidemic, which has its particularity. Product innovation is seriously insufficient. Great progress has been made in design technology, but there are still few achievements in product innovation. Generally speaking, it has not got rid of following and imitating. In most cases, it follows others, and its product innovation ability is not strong and its competitiveness is weak. At the same time, it also faces serious problems such as insufficient investment in R&D and serious shortage of talents.

Another important problem is that the low industrial concentration has not been improved. In 2020, the sales of 289 enterprises exceeded the threshold of 100 million yuan, accounting for 13% of the number of integrated circuit design enterprises in China, accounting for 79.9% of the total sales of the whole industry, reflecting the slow increase of industrial concentration to a certain extent. But, the proportion of the total sales of the top ten design enterprises in the total sales of the whole industry has once again dropped below 50%, and the threshold for entering the top ten design enterprises has not increased; The sum of sales of the three largest communication chip companies has not improved significantly; The layout of multimedia chips remains basically unchanged; Although consumer electronic chips occupy the second place in total, But there are no prominent leading enterprises.

With the rapid development of China's economy and the rise of strategic emerging industries, the integrated circuit industry will gain a broader market and innovation space, and there will be more market demand. At present, the integration and merger between domestic and foreign integrated circuit industries are constantly emerging. As China's market position continues to improve and the industrial base continues to mature, more overseas companies will choose to enter the Chinese market through mergers and acquisitions. China's integrated circuit design companies will increase their integration and reorganization efforts in the future to build large enterprises and leading enterprises.

In 2019, the scale of China's integrated circuit design industry reached 306.35 billion yuan. According to the statistics of China Semiconductor Industry Association, the annual sales revenue of the national integrated circuit design industry reached 377.84 billion yuan in 2020, an increase of 23.3% over 2019, and the industrial scale accounted for 42.7% of the national integrated circuit industry.; According to the historical growth rate of the domestic IC design market, by 2026, the scale of domestic IC design market is expected to exceed 1,000 billion yuan.

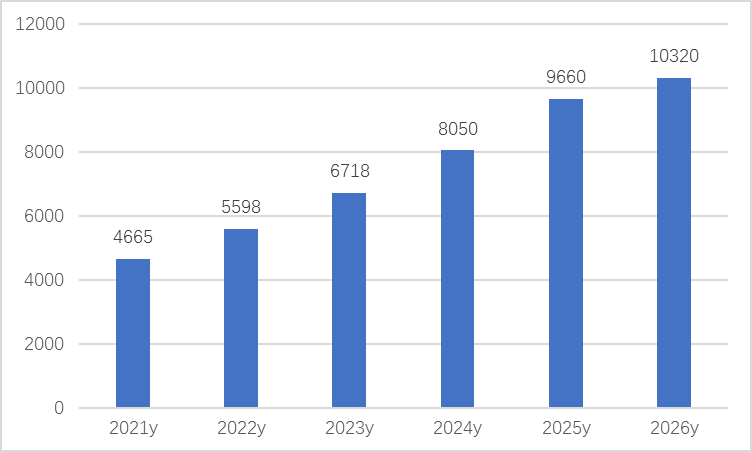

Figure 8.

China's IC design industry 2021-2026 market forecast (100 million yuan). [2] Analysis of Market Status and Competition Pattern of China's IC Design Industry in 2021 Huawei HiSilicon leads domestic development

[3] Analysis of the Development Status and Regional Competition Pattern of China's IC Design Industry in 2020; First-tier cities lead the way

[4] Analysis of the Present Situation and Competition Pattern of the National IC Design Industry in 2020 Shenzhen's market scale ranks first in the national cities

[5] Analysis of China's Integrated Circuit Development Status and Future Trends

[7] Development Status, Opportunities and Challenges of China's IC Design Industry

[8] Analysis on the Development of China's IC Design Industry in 2020

[9] The situation of China's integrated circuit design industry will be comprehensively combed in 2020

[10] Li ke. the development of China's integrated circuit industry ushered in a new climax [J]. internet economy, 2020(08):12-15.

Yin yayun. development prospect of China's IC design industry [J]. integrated circuit applications, 2020,37(04):128-129.

[12] Wang Longxing. Analysis of China's IC design industry in 2019 [J]. Integrated Circuit Application, 2020,37(02):1-3.

[13] Wei Shaojun. China's IC design industry market situation and thinking in 2019 [J]. electronic products world, 2019,26(12):19-23.

[14] Cai wenwei. analysis of the development status and countermeasures of integrated circuit design industry [J]. journal of science and technology economy, 2019,27(30):200-201.

[15] min gang. status analysis of China's integrated circuit design industry [J]. integrated circuit application, 2019,36(02):8-14